Choosing the right loan can have a long-term impact on your financial health. Whether you’re applying for a personal loan, mortgage, or auto loan, understanding how to compare loan interest rates is essential. Many borrowers make the mistake of focusing only on the monthly payment, but the interest rate determines how much you will ultimately pay over time.

In this comprehensive guide, you will learn how to compare loan interest rates effectively, understand key financial terms, and choose the best deal that aligns with your needs.

What Is a Loan Interest Rate?

A loan interest rate is the percentage charged by a lender for borrowing money. It represents the cost of borrowing and is typically expressed annually. The interest rate directly affects your monthly payments and the total repayment amount.

There are two main types of interest rates:

1. Fixed Interest Rate

A fixed interest rate remains the same throughout the life of the loan. This provides predictable monthly payments and stability.

2. Variable Interest Rate

A variable interest rate can change over time based on market conditions. While it may start lower than a fixed rate, it can increase, leading to higher payments.

Why Comparing Interest Rates Matters

Comparing interest rates is crucial because even a small difference can significantly affect your total repayment amount. For example, a 1% difference in interest on a large loan could cost you thousands over time.

Benefits of comparing loan rates include:

- Lower overall cost

- Better financial planning

- More favorable loan terms

- Reduced risk of overpaying

Key Factors to Consider When Comparing Loan Interest Rates

1. Annual Percentage Rate (APR)

The APR includes not only the interest rate but also fees and other costs associated with the loan. It provides a more accurate picture of the total cost.

2. Loan Term

The loan term refers to how long you have to repay the loan. Longer terms typically have lower monthly payments but higher total interest costs.

3. Fees and Charges

Look beyond the interest rate and consider additional fees such as:

- Origination fees

- Late payment penalties

- Prepayment penalties

4. Loan Type

Different loans have different rate structures. For example:

- Mortgages

- Personal loans

- Auto loans

Each has unique features that affect interest rates.

5. Credit Score

Your credit score plays a significant role in determining your interest rate. Higher scores typically qualify for lower rates.

Step-by-Step Guide to Comparing Loan Interest Rates

Step 1: Check Your Credit Score

Before applying for a loan, review your credit score. This helps you understand what rates you are likely to qualify for.

Step 2: Research Multiple Lenders

Do not settle for the first offer. Compare rates from banks, credit unions, and online lenders.

Step 3: Compare APR, Not Just Interest Rate

Always compare APR to get a true cost comparison.

Step 4: Evaluate Loan Terms

Consider repayment flexibility, penalties, and benefits.

Step 5: Use Loan Calculators

Online calculators help estimate monthly payments and total costs.

Fixed vs Variable Rates: Which Is Better?

Choosing between fixed and variable rates depends on your financial situation.

Fixed Rate Advantages

- Predictable payments

- Protection from rate increases

Variable Rate Advantages

- Lower initial rates

- Potential savings if rates drop

When to Choose Fixed

- Long-term loans

- Stable budgeting needs

When to Choose Variable

- Short-term loans

- Expectation of stable or falling rates

Common Mistakes to Avoid

1. Ignoring APR

Many borrowers focus only on the interest rate and overlook fees.

2. Choosing Based on Monthly Payment Alone

Lower payments often mean longer terms and higher total costs.

3. Not Reading the Fine Print

Hidden fees and conditions can increase costs.

4. Failing to Shop Around

Not comparing multiple lenders can lead to missed opportunities.

Tips for Getting the Best Loan Deal

Improve Your Credit Score

Pay bills on time and reduce debt before applying.

Consider a Shorter Loan Term

Shorter terms usually offer lower interest rates.

Negotiate with Lenders

Do not hesitate to ask for better terms.

Make a Larger Down Payment

This reduces the loan amount and risk for lenders.

Online Tools for Comparing Loan Rates

There are many online tools that allow you to compare loan rates easily. These tools provide side-by-side comparisons, helping you evaluate different options quickly.

Features to look for:

- Real-time rate updates

- Personalized offers

- Transparent fee breakdown

How Interest Rates Affect Monthly Payments

Higher interest rates increase your monthly payment and total repayment amount. Understanding this relationship helps you make better decisions.

For example:

- Higher rate = higher monthly payment

- Lower rate = lower total cost

Understanding Amortization

Amortization refers to how loan payments are applied over time. Early payments go mostly toward interest, while later payments reduce the principal.

Understanding amortization helps you see the true cost of borrowing.

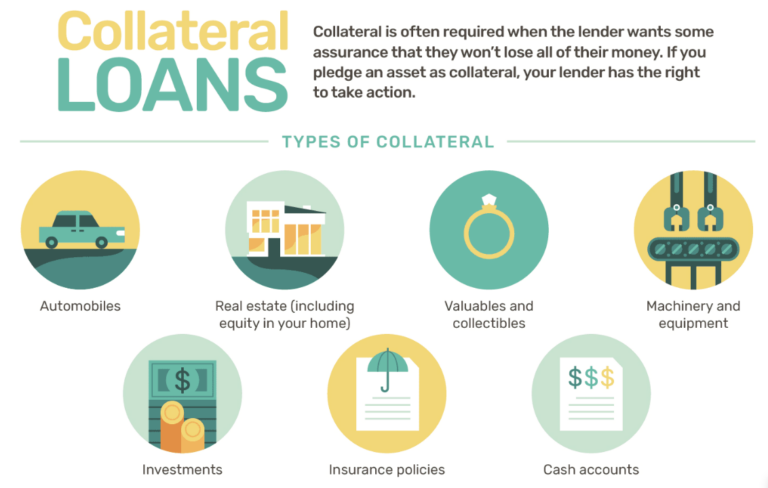

Secured vs Unsecured Loans

Secured Loans

Require collateral and typically offer lower interest rates.

Unsecured Loans

Do not require collateral but often have higher rates.

Choosing between the two affects your interest rate and risk level.

The Role of Market Conditions

Interest rates are influenced by economic factors such as inflation, central bank policies, and market demand. Keeping an eye on trends can help you choose the right time to borrow.

Refinancing as a Strategy

If you already have a loan, refinancing can help you secure a lower interest rate. This can reduce monthly payments or shorten the loan term.

When to Lock in an Interest Rate

Rate locks are common in mortgages. Locking in a rate protects you from increases during the approval process.

Final Checklist Before Choosing a Loan

Before making a final decision, ask yourself:

- What is the APR?

- Are there hidden fees?

- Is the loan term suitable?

- Can I afford the monthly payments?

Conclusion

Comparing loan interest rates is a critical step in making a smart financial decision. By understanding key factors such as APR, loan terms, and fees, you can avoid costly mistakes and choose the best deal.

Take your time, research thoroughly, and use available tools to ensure you select a loan that fits your financial goals. The right choice today can save you money and stress in the future.

Frequently Asked Questions (FAQs)

What is the difference between APR and interest rate?

APR includes both the interest rate and additional fees, while the interest rate only reflects the cost of borrowing.

How can I get the lowest interest rate?

Improve your credit score, compare lenders, and consider shorter loan terms.

Is a lower interest rate always better?

Not necessarily. You must consider fees, loan terms, and overall cost.

Can I negotiate loan interest rates?

Yes, many lenders are open to negotiation, especially if you have a strong credit profile.